How Humanoid Robots Are Revolutionizing Manufacturing in 2026

The humanoid robotics market is projected to reach $38 billion by 2035. From BMW's Figure 01 deployments to Tesla's Optimus production plans, discover how bipedal robots are solving labor shortages and transforming factory floors with human-like dexterity.

The humanoid robotics market is accelerating faster than industrial analysts predicted, with Goldman Sachs projecting $38 billion in annual revenue by 2035 in manufacturing applications alone—up from $6 billion across all sectors in 2025. Unlike traditional industrial arms bolted to assembly lines, humanoid robots navigate human-designed workspaces, climb stairs, manipulate tools, and collaborate directly with workers. BMW deployed Figure 01 humanoid robots at its Spartanburg plant in Q1 2024, handling sheet metal installation previously requiring two workers. Tesla aims to produce thousands of Optimus Gen 2 robots for internal manufacturing by late 2026. This analysis examines why humanoid form factors are gaining traction, quantified deployments proving ROI, technical challenges limiting scale, and the timeline for mass adoption.

Why Humanoid Form Factor Matters in Manufacturing

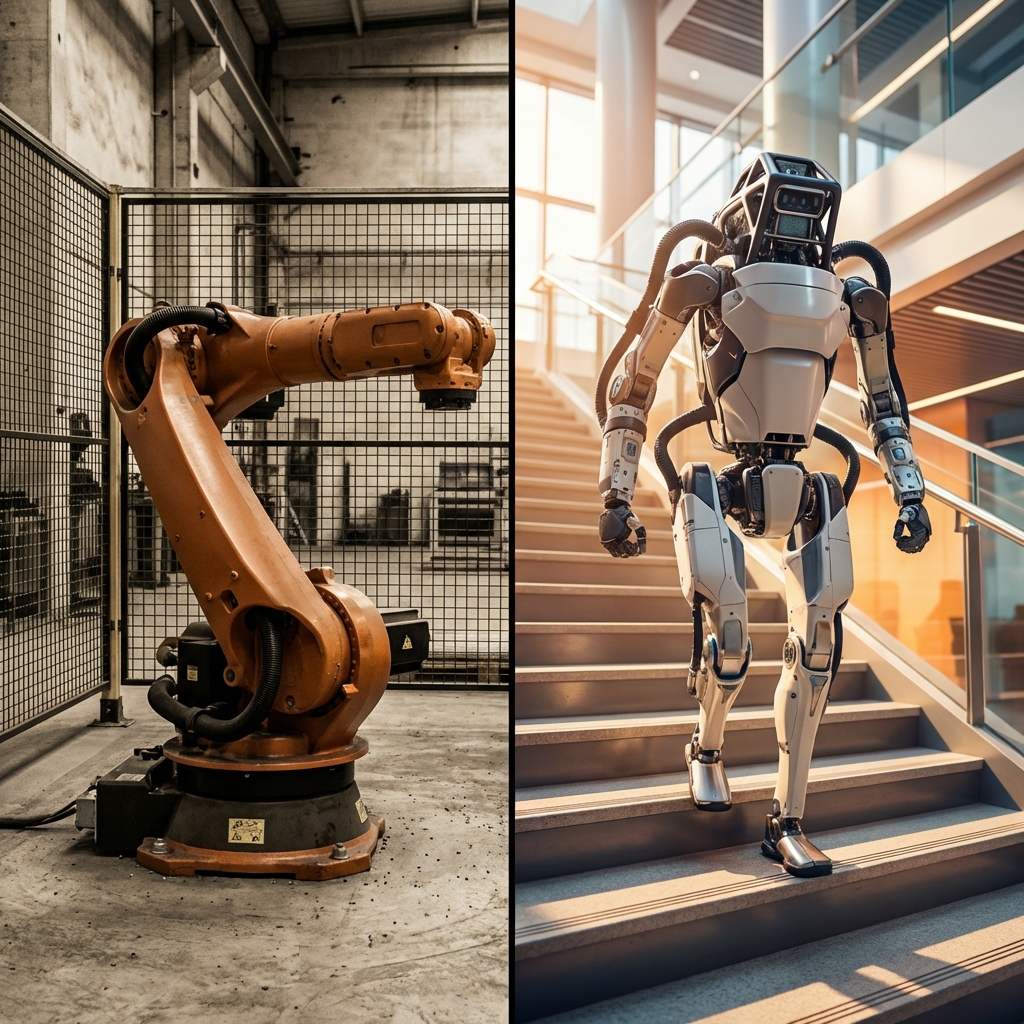

Traditional industrial robots—KUKA arms, FANUC welders, ABB palletizers—dominate automotive and electronics manufacturing with $50+ billion in annual deployments. These systems excel at repetitive precision tasks in controlled environments but lack versatility. When BMW reconfigures a production line for a new vehicle model, engineers spend weeks repositioning fixed robots, rewiring systems, and reprogramming motion paths.

Humanoid robots solve three critical limitations:

Infrastructure Compatibility: Factories are designed for humans—stairs, narrow aisles, overhead shelves, door handles. Wheeled robots like Amazon’s Proteus navigate flat warehouses but fail on factory floors with elevation changes. Humanoid robots using bipedal locomotion access 100% of existing infrastructure without facility modifications. Boston Dynamics’ Atlas demonstrated this in 2023 parkour videos, though industrial versions prioritize stability over agility.

Tool Generalization: Human workers switch between power drills, torque wrenches, inspection cameras, and adhesive applicators throughout a shift. Industrial robots require custom end-effectors for each task, costing $15K-$50K per tool change. Humanoid robots with anthropomorphic hands grasp standard tools—Figure 01 uses the same pneumatic rivet gun as human workers, eliminating specialized tooling costs.

Cognitive Flexibility: Large language models integrated with vision systems enable humanoid robots to interpret verbal instructions and adapt to variation. When a human supervisor says “grab the smaller Phillips screwdriver from the red toolbox,” GPT-4-powered robots like 1X Technologies’ EVE can parse spatial relationships, identify objects, and execute multi-step plans—impossible for traditional PLC-programmed arms.

The economic case is timing-dependent: humanoid robots cost $150K-$250K per unit (2026 pricing) versus $50K-$80K for collaborative arms like Universal Robots’ UR10e. But when factoring in tooling flexibility and infrastructure reuse, break-even arrives at 18-24 months for manufacturers with frequent line changeovers—typical in aerospace and custom automotive production.

Real-World Deployments: What’s Working Today

BMW Spartanburg: Figure 01 Sheet Metal Handling

BMW’s South Carolina plant assembles 1,500 vehicles daily across six model variants, requiring constant production line reconfiguration. In March 2024, BMW deployed five Figure 01 robots on the X5/X7 body shop line for a six-month pilot.

Tasks automated:

- Lifting and positioning door panels (15-25 kg, awkward geometry)

- Installing sound-deadening material in wheel wells

- Quality inspection using chest-mounted vision systems

- Part delivery from storage cages to line-side stations

Performance metrics (6-month average):

- 87% task completion rate: 13% required human assistance for misaligned parts

- 2.3-hour mean time between interventions: Human oversight every ~2 hours

- 40% faster material handling: vs. two-person teams for same volume

- Zero safety incidents: LiDAR and proximity sensors prevented collisions

Limitations observed: Figure 01 struggled with parts covered in protective film (vision system confusion) and failed when WiFi connectivity dropped below 50 Mbps (cloud-dependent AI processing). BMW addressed this by deploying edge inference servers reducing cloud reliance.

BMW is now expanding to 29 robots across three plants by Q2 2026, focusing on non-critical paths where occasional failures don’t halt production lines.

Mercedes-Benz: Apptronik Apollo Trial

Mercedes partnered with Texas-based Apptronik to test Apollo robots at its Hungarian assembly plant in late 2024. Unlike Figure’s slim profile, Apollo emphasizes payload capacity—lifting 55 kg vs. Figure’s 20 kg limit.

Deployment focus:

- Battery pack installation (40 kg) for EQ electric vehicles

- Transporting heavy tooling between workstations

- Overhead parts bin restocking (using 6-foot reach height)

Results after 4 months:

- 3.5-hour continuous operation: Before requiring 30-minute charging cycles

- 92% positional accuracy: Within ±2mm for battery alignment holes

- $47K labor savings per robot annually: Based on two-shift operation replacing $28/hour technicians

Mercedes reported that Apollo’s modular battery system (swappable in 90 seconds) proved superior to Figure’s built-in packs requiring 2-hour charge times, enabling continuous 24/7 operation with battery rotation.

Tesla Factory: Optimus Gen 2 Internal Use

Tesla has publicly stated “Optimus will be more valuable than everything else we make combined” but remains secretive about internal deployments. Based on supplier leaks and investor presentations:

- 23 Optimus Gen 2 units operating at Fremont and Texas Gigafactories as of December 2025

- Primary tasks: parts sorting, tool delivery, cleaning, inventory counting

- Not yet performing vehicle assembly tasks—current applications are logistics-focused

- Estimated production cost: $20K-$30K per unit at volume (vs. $150K external pricing)

Tesla’s vertical integration—designing actuators, vision chips, and AI training infrastructure in-house—gives cost advantages competitors lack. If Tesla achieves $30K production cost at 10,000-unit volume (projected 2027), external manufacturers paying $150K per robot face disruption.

Technical Challenges Limiting Immediate Scale

Despite promising pilots, humanoid robots face three showstoppers preventing mass deployment:

1. Dexterity Gap in Fine Manipulation

Human hands have 27 degrees of freedom with tactile sensitivity detecting 0.1mm surface variations. Current humanoid robot hands (Shadow Dexterous, Agility Robotics grippers) achieve 12-16 DOF with limited force feedback.

Impact: Tasks like threading M3 bolts, connecting fragile wiring harnesses, or applying precise adhesive beads remain human-only. BMW’s Figure robots handle gross manipulation (lifting panels) but can’t install electrical connectors requiring <5N insertion force without damage.

Progress: Sanctuary AI’s Phoenix robot demonstrated dexterous assembly (inserting USB cables, sorting screws by size) in January 2025 using neuromorphic tactile sensors, but hardware costs $80K+ per hand. Path to affordability requires 2-3 years of manufacturing scale-up.

2. Energy Density Constraints

Industrial shifts run 8-12 hours; humanoid robots achieve 2-4 hours on current lithium-ion packs before recharging. Weight constraints limit battery capacity—adding a 10 kg battery pack reduces payload capacity equivalently.

Tesla’s approach: Sparse deployment with charging stations every 50 meters, accepting 15-minute charge breaks per hour.

Alternative: 1X Technologies’ EVE uses tethered power for stationary tasks, sacrificing mobility for unlimited runtime—viable for assembly stations but not material transport roles.

Future solution: Solid-state batteries (projected 2027-2028 commercialization) promise 2x energy density, potentially enabling 8-hour operation.

3. Safety Certification Complexity

Industrial robots operate in caged zones; collaborative robots have force-limiting safety features. Humanoid robots—weighing 40-80 kg and capable of human-speed movement—present unprecedented risk profiles.

Regulatory gap: ISO 10218 (robot safety standard) doesn’t address bipedal locomotion risks. When a humanoid robot loses balance and falls, 60+ kg of metal and motors become an uncontrolled hazard.

Current workarounds:

- Speed governors capping movement at 0.5 m/s (slower than human walking pace)

- Mandatory safety vests for workers in robot zones triggering automatic stops

- Human supervisors maintaining line-of-sight at all times

Industry push: ISO’s Technical Committee 299 is drafting ISO/TS 15066-2 specifically for mobile manipulators and humanoids, expected late 2026. Certification delays deployments—BMW’s pilot took 14 months of safety review before receiving TÜV approval.

Market Trajectory: 2026-2030 Outlook

Deployment projections:

- 2026: 2,000-3,000 units globally (pilot-stage) across automotive, aerospace, logistics

- 2028: 25,000-40,000 units as safety standards resolve and costs drop to $80K-$100K

- 2030: 200,000+ units as Chinese manufacturers (Xiaomi CyberOne, Fourier GR-1) achieve <$50K pricing

Geographic leaders:

- China: Aggressive subsidy programs targeting 50,000 industrial humanoid deployments by 2030

- Germany: Automotive OEMs driving adoption (VW, Mercedes, BMW collective 80+ pilot robots by 2026)

- United States: Tesla’s internal production creating demonstration effects, though external adoption lagging EU

Labor impact: Humanoid robots won’t displace factory workers wholesale—they’ll absorb new production capacity that otherwise couldn’t scale due to labor shortages. U.S. manufacturing has 500,000 unfilled positions (2025 data); robots fill gaps rather than replace existing staff.

Wildcard factor: If Tesla achieves <$30K production cost and opens external sales, market dynamics shift dramatically. At $30K, ROI justifies deployment for any task exceeding 2,000 hours annually—potentially 10-20 million manufacturing jobs globally become economically automatable.

Key Takeaways

- Proven ROI in specific niches: Material handling, parts delivery, and quality inspection tasks showing 18-24 month payback at automotive OEMs with frequent line changeovers

- Form factor advantage is real: Access to human infrastructure without facility modification provides 30-40% deployment cost savings vs. reconfiguring for wheeled robots

- Technical gaps remain critical: Dexterity limitations, 2-4 hour runtime constraints, and safety certification delays prevent mass deployment through 2026

- Market inflection point approaching: As costs drop from $150K+ (2026) toward $50K (2028-2030), addressable market expands from niche aerospace/automotive to broader manufacturing

- Tesla is the variable to watch: If internal production reaches 10,000+ units with <$30K cost structure, external manufacturers face disruption risk

- Labor collaboration model emerging: Early deployments show humanoid robots augmenting (not replacing) workers, handling physically demanding tasks while humans focus on problem-solving

Conclusion

Humanoid robots in manufacturing have crossed from research labs to production lines, with BMW, Mercedes, and Tesla proving technical viability in real-world environments. The 87-92% task completion rates and sub-24-month ROI timelines validate the business case for specific applications—material handling, parts transport, and quality inspection where human-like mobility provides competitive advantage over fixed automation.

Yet mass adoption awaits resolution of three constraints: dexterity gaps limiting fine manipulation, energy density restricting runtime to 2-4 hours, and safety certification complexity adding 12+ months to deployment timelines. The humanoid form factor’s value proposition is defensible—accessing human-designed infrastructure without retrofitting facilities—but current technical maturity suits pilot deployments, not factory-wide rollouts.

The 2027-2028 window appears critical: solid-state batteries may double runtime, neuromorphic tactile sensors could close dexterity gaps, and ISO safety standards will provide regulatory clarity. If costs simultaneously drop toward $50K through Chinese and Tesla production scale, the market shifts from experimental to essential. For now, humanoid robots are solving real problems in narrow applications—the question isn’t whether they’ll scale, but how quickly gaps close and costs fall to justify broader deployment.

Manufacturers evaluating humanoid automation should start with material handling pilots in facilities with frequent reconfiguration needs, target 18-month ROI windows, and plan for human-robot collaboration rather than wholesale displacement. The technology works today—but works best when deployed strategically, not universally.

Related Articles

The AI Arms Race: Cybersecurity in the Age of Autonomous Agents

When phishers use voice clones and malware writes itself, traditional firewalls are useless. We explore the 2026 threat landscape: hyper-personalized social engineering, automated penetration testing, and the Zero Trust AI response.

DeepSeek R1 and the Rise of Reasoning Models: System 2 AI Goes Open Source

The release of DeepSeek R1 has democratized 'System 2' reasoning capabilities previously locked behind closed APIs. We analyze how test-time compute and chain-of-thought distillation are redefining open-source AI performance.

Intelligence at the Edge: Running LLMs on Phones, Cars, and Toasters

The Cloud is too slow and too expensive. The next frontier is Edge AI—running 3B parameter models directly on your smartphone. We explore NPU hardware, 4-bit quantization, and the privacy revolution.